Understanding the world of finance can often feel like learning a foreign language. However, mastering basic financial concepts is essential for anyone looking to build a secure and prosperous future. Financial literacy provides the tools necessary to make informed decisions about spending, saving, and investing. Without these fundamentals, it is easy to fall into debt traps or miss out on opportunities for wealth creation. This guide breaks down complex terms into simple, actionable insights for beginners.

The Power of Budgeting

At its core, budgeting is the practice of creating a plan for your money. It is not about restricting your lifestyle but about gaining control over where your hard-earned cash goes. Common budgeting strategies include:

- The 50/30/20 Rule

- Zero-Based Budgeting

- The Envelope System

By tracking every dollar, you can ensure that your essential needs are met while still setting aside funds for your future goals.

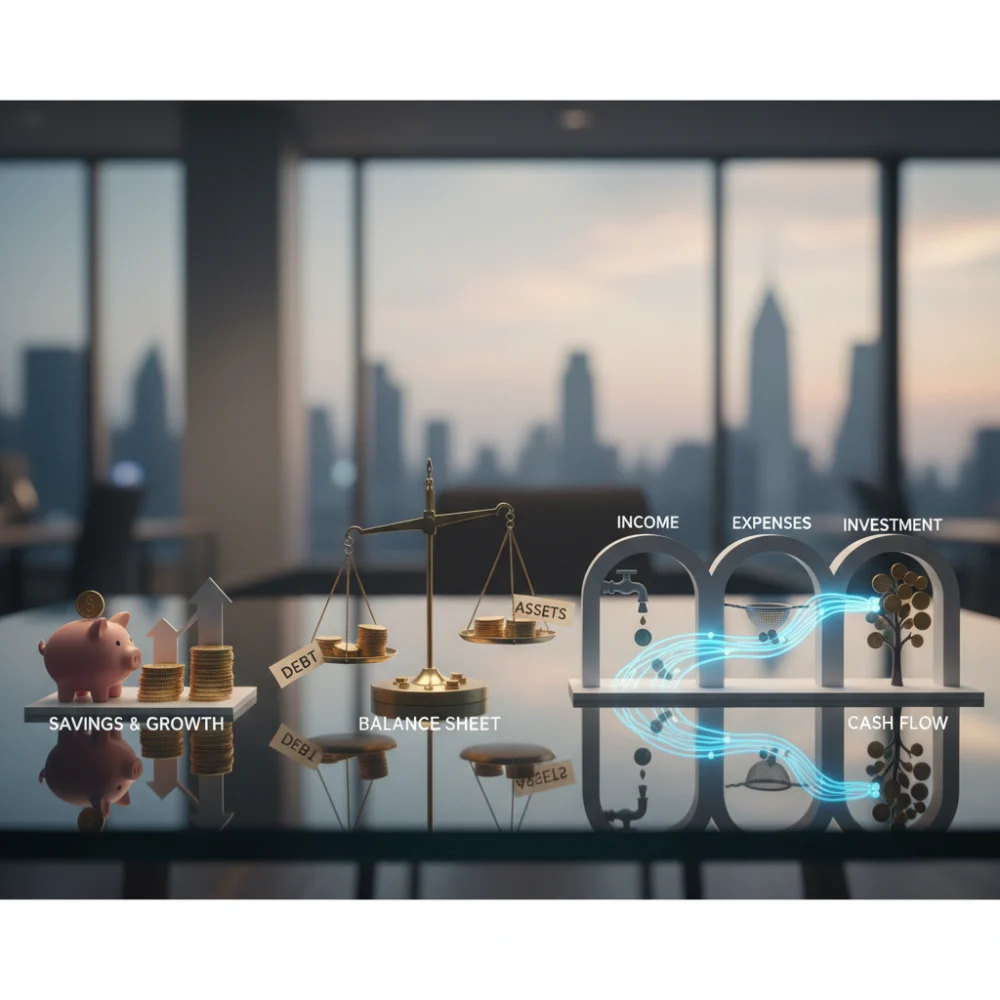

Income vs. Expenses

The relationship between income and expenses is the most basic equation in finance. Income includes all the money you receive, such as salary, bonuses, or side hustle earnings. Expenses are everything you spend money on, from rent and groceries to entertainment. To build wealth, your income must consistently exceed your expenses. This surplus is what allows you to invest and grow your net worth over time.

Assets vs. Liabilities

Understanding the difference between an asset and a liability is a game-changer. Simply put, an asset is something that puts money into your pocket, such as stocks, real estate, or a business. A liability is something that takes money out of your pocket, such as car loans, credit card debt, or high-interest personal loans. The goal of financial independence is to accumulate assets that generate enough income to cover your liabilities and lifestyle.

Building an Emergency Fund

An emergency fund is a dedicated savings account meant to cover unexpected life events, such as medical emergencies or job loss. Most experts recommend saving three to six months worth of living expenses. Having this safety net prevents you from dipping into your long-term investments or taking on high-interest debt when a crisis occurs. It provides peace of mind and financial stability during turbulent times.

The Magic of Compound Interest

Albert Einstein famously called compound interest the eighth wonder of the world. It refers to the interest you earn on your initial investment plus the interest that has accumulated over time. This creates a snowball effect where your money grows exponentially. The key to maximizing compound interest is time; the earlier you start investing, the more time your money has to grow, even if the initial amounts are small.

Managing Debt Effectively

Not all debt is created equal. Good debt is typically used to purchase something that increases in value or generates income, like a mortgage for a home or a student loan for a high-earning degree. Bad debt, on the other hand, involves borrowing money for depreciating assets or consumption, such as high-interest credit card debt. Managing debt involves prioritizing the repayment of high-interest loans while maintaining a healthy credit utilization ratio.

Understanding Inflation

Inflation is the gradual increase in the prices of goods and services over time, which reduces the purchasing power of your money. For example, a dollar today will likely buy less ten years from now. To combat inflation, it is important to invest your money in assets that have the potential to grow faster than the inflation rate. Keeping all your savings in a low-interest bank account can actually result in losing wealth in real terms over the long run.

Risk vs. Reward

In the world of investing, risk and reward are inextricably linked. Generally, the higher the potential return on an investment, the higher the risk involved. For instance, stocks offer higher potential returns than savings accounts but come with the risk of market volatility. Understanding your personal risk tolerance—how much loss you can stomach—is crucial when building an investment portfolio that aligns with your financial goals.

The Importance of Diversification

Diversification is the strategy of spreading your investments across various asset classes, such as stocks, bonds, and real estate, to reduce risk. The logic is simple: if one investment performs poorly, others may perform well, balancing out your overall portfolio. Diversification protects you from the total loss that could occur if you put all your money into a single company or sector. It is one of the few free lunches in finance.

Calculating Your Net Worth

Your net worth is a snapshot of your financial health at a specific point in time. It is calculated by subtracting your total liabilities from your total assets. Tracking your net worth annually or quarterly allows you to see the progress you are making toward your financial goals. A growing net worth indicates that you are either increasing your assets, decreasing your debts, or both, which is the ultimate sign of financial success.

Planning for Retirement

Retirement planning is the process of setting aside funds today to support yourself when you stop working. It involves utilizing tax-advantaged accounts like a 401(k) or an IRA. The goal is to accumulate a nest egg large enough to sustain your lifestyle for decades. Because of the power of compounding, starting your retirement contributions in your 20s or 30s is significantly more effective than starting in your 40s or 50s.

The Role of Credit Scores

A credit score is a numerical representation of your creditworthiness. Lenders use this score to determine whether to approve you for loans. Key factors that influence your score include:

- Payment history

- Total amount of debt

- Length of credit history

- New credit inquiries

Maintaining a good score involves paying bills on time, keeping credit card balances low, and avoiding excessive new credit applications to ensure you have access to the best financial products.

Tax Literacy and Efficiency

Understanding how taxes affect your finances is crucial for maximizing your wealth. Tax literacy involves knowing which investments are tax-deductible or tax-deferred. By using legal strategies to minimize your tax liability, you can keep more of your earnings for reinvestment. This might include contributing to retirement accounts or holding investments for more than a year to qualify for lower long-term capital gains tax rates.

Developing a Financial Mindset

Beyond the numbers, financial success requires a disciplined mindset. This means delaying gratification, avoiding lifestyle creep, and staying committed to your long-term plan even during market downturns. Financial literacy is a lifelong journey of learning and adaptation. By mastering these basic concepts, you are taking the first and most important step toward achieving financial freedom and long-term security.

{kind=link}