The Fundamental Philosophy of Debt as a Financial Tool

In the world of personal finance, debt is often viewed with fear, yet it remains one of the most powerful tools for wealth creation when used correctly. The primary distinction between good debt and bad debt lies in the Return on Investment (ROI). Good debt is an investment that will grow in value or generate even more income over the long term. Bad debt, on the other hand, is used to purchase things that lose value quickly or provide no financial return, often at a high cost due to compounding interest.

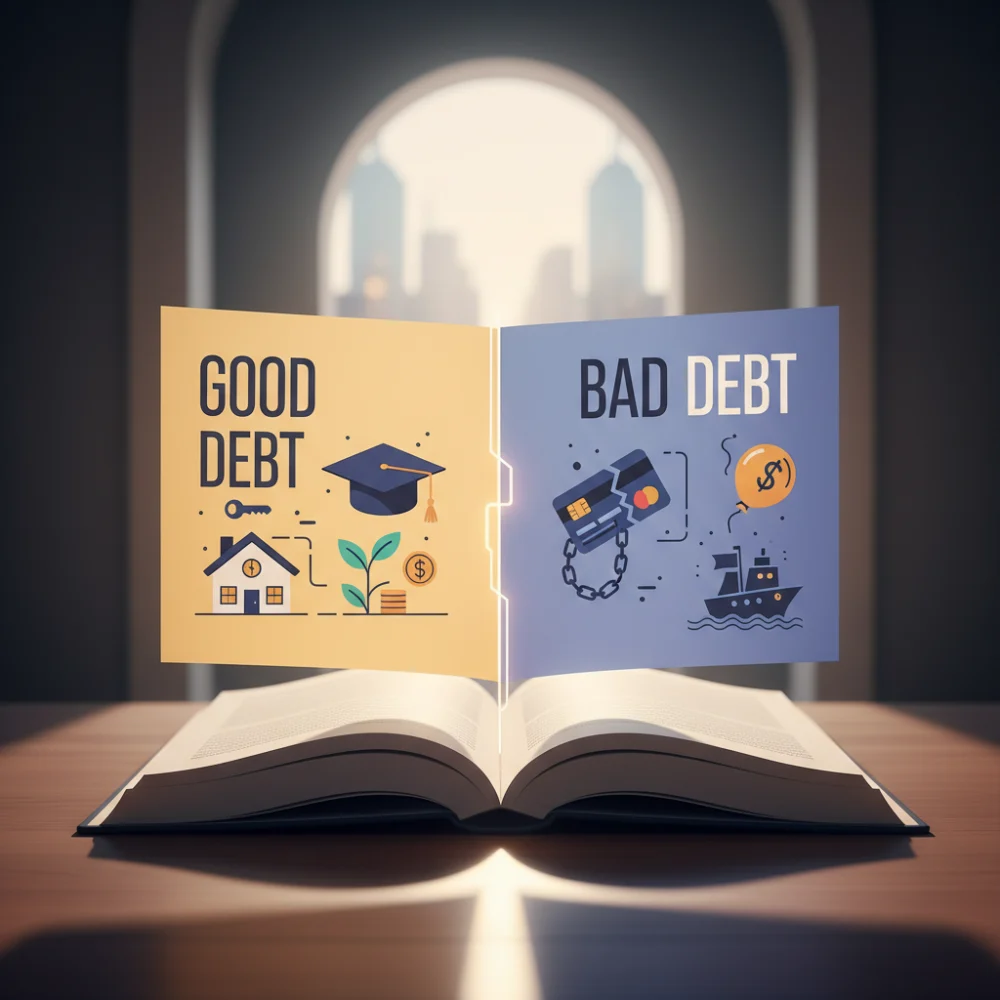

Defining Good Debt: An Investment in Your Future

Good debt is generally characterized by low interest rates and the potential to increase your net worth. It is a strategic move where the borrower expects the benefit of the loan to outweigh the cost of the interest. By using leverage, individuals can acquire assets that they otherwise could not afford upfront, allowing those assets to appreciate over time. This category of debt is considered constructive because it builds a foundation for future financial stability and growth.

Real Estate and Mortgages: The Classic Good Debt

A mortgage is perhaps the most common example of good debt. For most people, a home is the largest asset they will ever own. While you pay interest on the loan, real estate historically appreciates in value over several decades. Furthermore, homeownership provides stability and can offer tax advantages in many jurisdictions. If the property is used as a rental, the debt becomes even more efficient as the tenant’s rent covers the mortgage payments, effectively building your equity for free.

Education Loans: Investing in Human Capital

Student loans are frequently classified as good debt because education is an investment in human capital. Statistically, individuals with higher levels of education or specialized certifications tend to earn significantly more over their lifetime than those without. While the initial debt may seem daunting, the increased earning potential usually provides a high return on the investment, making it a sensible financial decision for many career paths.

Business Loans: Leveraging for Growth

Taking out a loan to start or expand a business is another form of good debt. If the business is successful, the profits generated will far exceed the interest paid on the loan. Entrepreneurs use debt to fund inventory, marketing, or equipment that directly contributes to revenue generation. However, this requires a solid business plan and market validation to ensure that the debt remains productive rather than a burden.

Identifying Bad Debt: The Drain on Your Wealth

Bad debt is characterized by high interest rates and the consumption of non-essential goods. This type of debt is often used to fund a lifestyle that the borrower cannot currently afford. Unlike good debt, bad debt does not provide a path to increased wealth; instead, it creates a cycle of monthly payments that reduce your disposable income and prevent you from saving or investing for the future. Recognizing bad debt is the first step toward achieving financial freedom.

The Danger of High-Interest Credit Card Debt

Credit card debt is the most prevalent form of bad debt. Because credit cards often carry double-digit interest rates, carrying a balance can be financially devastating. When you use a credit card for daily expenses or luxury items and do not pay it off in full, you are essentially paying significantly more for those items than their actual price tag. This type of debt is regressive and can quickly spiral out of control if not managed with strict discipline.

Payday Loans and Predatory Lending Practices

Perhaps the most extreme form of bad debt is the payday loan. These loans are designed to bridge the gap until the next paycheck but come with astronomical interest rates and fees. They often target vulnerable populations and create a debt trap where the borrower must take out new loans to pay off old ones. Avoiding these types of high-cost, short-term loans is essential for maintaining financial health.

Consumerism and Depreciating Assets

Using debt to purchase consumer goods like the latest electronics, designer clothing, or expensive furniture is a hallmark of bad debt. These items lose value the moment they are purchased and do not contribute to your financial growth. When you borrow money for consumption, you are essentially borrowing from your future self to pay for a temporary pleasure today, which is a losing strategy in the long run.

The Nuance of Auto Loans: A Grey Area

Car loans sit in a grey area between good and bad debt. On one hand, a reliable vehicle may be necessary to get to work and earn a living, making it a functional necessity. On the other hand, cars are depreciating assets that lose value rapidly. A modest loan for a reliable used car might be considered a necessary expense, but taking a high-interest loan for a luxury vehicle far beyond your needs is definitely categorized as bad debt.

The Role of Interest Rates in Debt Classification

The interest rate is a critical factor in determining whether debt is manageable or toxic. Even a loan for a productive purpose can become bad debt if the interest rate is too high. High interest rates eat into your potential profits or savings, making it harder to pay down the principal balance. Financial experts often suggest prioritizing the repayment of any debt with an interest rate above 7-8%, as it is difficult to find investments that consistently beat that cost of capital.

Understanding Your Debt-to-Income Ratio

To manage debt effectively, you must understand your Debt-to-Income (DTI) ratio. This is the percentage of your gross monthly income that goes toward paying debts. Lenders use this ratio to determine your creditworthiness. A low DTI ratio indicates that you have a good balance between debt and income, while a high ratio suggests that you are overextended. Keeping your DTI within a healthy range (usually below 36%) is vital for maintaining a strong financial profile.

Strategies for Eliminating Bad Debt

If you find yourself burdened by bad debt, several strategies can help you regain control. The Debt Avalanche method involves paying off debt with the highest interest rates first, which saves the most money over time. Alternatively, the Debt Snowball method focuses on paying off the smallest balances first to build psychological momentum. Both strategies require a strict budget and a commitment to stop accumulating new debt while paying off the old.

Leveraging Good Debt Responsibly

Even good debt carries risk. Over-leveraging, even for assets like real estate or business, can lead to financial ruin if the market shifts or income streams dry up. It is important to have a safety net or emergency fund in place before taking on significant good debt. Responsible borrowing means ensuring that you can still meet your obligations even if your primary income source is temporarily interrupted.

The Psychological Impact of Debt Management

The way we manage debt has a profound impact on our mental well-being. Bad debt often leads to stress, anxiety, and a feeling of being trapped. In contrast, managing good debt effectively can provide a sense of empowerment and progress. By shifting your mindset to view debt as a strategic tool rather than a burden, you can make more informed decisions that align with your long-term life goals.

Conclusion: Building a Path to Financial Literacy

In conclusion, the essential understanding of good debt vs. bad debt is about more than just numbers; it is about intentionality. Use debt to buy assets, not liabilities. Prioritize low-interest investments over high-interest consumption. By applying these principles, you can navigate the complex world of finance with confidence, ensuring that every dollar you borrow is working toward building a wealthier and more secure future for yourself and your family.

{kind=link}