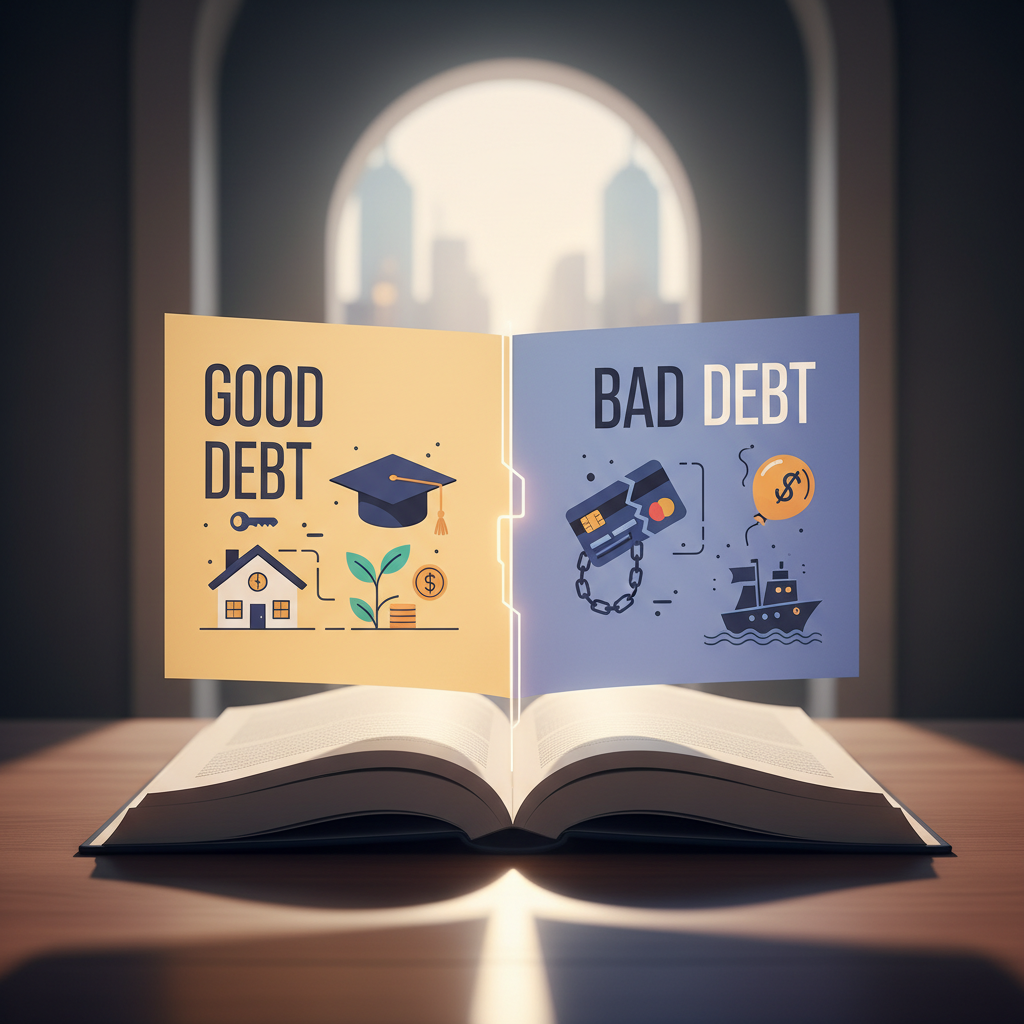

Debt consolidation is a financial strategy that involves combining multiple high-interest debts into a single, more manageable payment. This process is often used to secure a lower interest rate, reduce monthly payments, or simplify the repayment process. By understanding the nuances of how debt consolidation works, you can take a significant step toward achieving financial stability and long-term freedom from the burden of owing money.

Understanding the Core Concept of Consolidation

At its heart, debt consolidation is about restructuring your liabilities. Instead of juggling various due dates and interest rates from credit cards, medical bills, or personal loans, you take out a new loan to pay them all off. This leaves you with just one creditor and one monthly obligation, which can significantly reduce the stress associated with managing complex finances.

Assessing your current financial situation is the first critical step. Before applying for any new credit product, you must have a clear picture of exactly how much you owe, the interest rates on each account, and your current monthly minimum payments. Without this data, it is impossible to determine if a consolidation plan will actually save you money or simply move the debt around.

The Benefit of Lower Interest Rates

The primary goal of wise debt consolidation is to lower the overall cost of borrowing. If you are paying 20% interest on several credit cards and can qualify for a consolidation loan at 10%, you will save a substantial amount of money over the life of the loan. This reduction in interest allows more of your monthly payment to go toward the principal balance rather than just covering the cost of borrowing.

Using a personal loan for debt consolidation is one of the most common methods. These loans typically offer fixed interest rates and set repayment terms, usually ranging from two to seven years. Because the payments are predictable, it becomes much easier to plan your budget and see exactly when you will be debt-free, provided you do not accrue new charges on your original accounts.

Exploring Balance Transfer Credit Cards

Another popular option is the balance transfer credit card, which often features an introductory period of 0% APR. This can be an incredibly powerful tool if you can pay off the entire balance within the promotional window, which usually lasts between 12 and 21 months. However, you must be wary of balance transfer fees, which typically range from 3% to 5% of the total amount transferred.

Homeowners might consider using a Home Equity Loan or Line of Credit (HELOC) to consolidate debt. Because these loans are secured by your property, they often carry much lower interest rates than unsecured personal loans. However, this strategy comes with significant risk; if you fail to make payments, you could face foreclosure and lose your home, making it a high-stakes decision that requires careful thought.

The Importance of Credit Score Impact

Consolidating debt can have a mixed impact on your credit score. Initially, applying for a new loan or credit card may cause a small, temporary dip due to a hard inquiry. However, in the long run, consolidation can improve your score by lowering your credit utilization ratio and establishing a history of consistent, on-time payments. It is vital to maintain these accounts without closing them immediately, as the length of credit history also factors into your score.

One of the biggest mistakes people make is falling into the trap of new debt. After paying off credit card balances with a consolidation loan, the temptation to use those now-empty cards can be overwhelming. If you continue to spend while paying off the consolidation loan, you will end up with twice as much debt. Wise consolidation requires a commitment to stop using credit cards for lifestyle expenses.

Creating a Strict Budget Post-Consolidation

Success in debt consolidation is heavily dependent on your behavior after the loan is secured. You must create a realistic budget that accounts for your new monthly payment while ensuring you have enough for savings and daily living expenses. Tracking every dollar spent will help you identify patterns that led to the initial debt and allow you to make necessary lifestyle adjustments.

If your credit score is too low to qualify for a traditional loan, a Debt Management Plan (DMP) through a non-profit credit counseling agency might be the best route. These agencies work with your creditors to lower interest rates and waive fees. You make one monthly payment to the agency, which then distributes the funds to your creditors. This does not involve taking out a new loan but still offers the benefits of consolidation.

Comparing Fees and Hidden Costs

Always read the fine print before signing any consolidation agreement. Some lenders charge origination fees, which are deducted from the loan amount before you receive it. Others may have prepayment penalties that punish you for paying off the debt early. By comparing the Annual Percentage Rate (APR), which includes both interest and fees, you can get a true sense of the cost of the consolidation option.

The psychological aspect of debt cannot be ignored. Consolidation can provide an immediate sense of relief, but it is important not to let that relief turn into complacency. Treat the consolidation as a tool, not a cure. The cure for debt is a fundamental shift in how you view and handle money, focusing on living within your means and prioritizing financial security over immediate gratification.

When to Seek Professional Advice

If you find yourself overwhelmed and unable to determine which consolidation path is right for you, seeking advice from a certified financial planner or a reputable credit counselor is wise. These professionals can provide personalized guidance based on your specific financial profile and help you avoid predatory lenders who target individuals in financial distress.

Ultimately, the goal of consolidating debt wisely is to create a sustainable path toward long-term financial habits. This includes building an emergency fund so that unexpected expenses do not force you back into debt. By combining the right financial products with disciplined spending and a clear repayment plan, you can regain control of your finances and build a more secure future.

Summary of Best Practices

- Review all loan terms carefully to ensure you are saving money.

- Automate your monthly payments to avoid late fees and penalties.

- Monitor your credit report regularly to track your progress and score.

- Avoid taking on new credit lines during the repayment period.